How to prepare for the Health & Social Care Levy

Now that we are beginning to see life slowly returning to normal, the time has come for both employees and employers to pay back into the system that supported us all through the pandemic, with this being specifically targeted to pay directly back into the NHS, health and social care systems.

The Health and Social Care Levy is being introduced from the 6th April 2022.

Tax year 2022-2023

Initially, the levy will be introduced by way of a 1.25% increase to Class 1, Class 1A and Class 1B National Insurance contributions.

This will mean that employees will see an increase in National Insurance deducted from their payslip, whilst employers will see an additional cost as well.

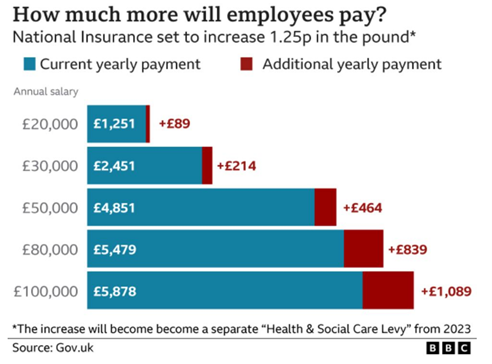

The graph below shows the impact the levy will have and how it will affect people based on their annual salary.

Graph taken from this article.

Alongside this, the government has requested that employers add a payslip message to their payslips to explain the increase in the National Insurance charges. This will allow employees to understand what the funds are being used for.

The message suggested to use is “1.25% uplift in NICs funds NHS, Health & Social Care”, but this can be tailored to each company’s wish as long as the message is clear to employees on what the increase is and what it is for.

Existing exemptions will still apply:

If an employee falls into any of the categories below and earns less than £50,270 (or £25,000 for Freeport employees) per year, then they will not have to pay the extra 1.25%

- Apprentices under the age of 25

- Employees under the age of 21

- Armed Forces veterans

- Employees in Freeports

As is currently the case, however, the employer will still be due to pay the extra 1.25%.

Tax year 2022-2023

Then from 6th April 2023, the National Insurance contributions will return to 2021-2022 levels and the levy will at this point become a separate new tax of 1.25%. Earnings on which National Insurance contributions are calculated will also be used to calculate the levy separately.

The levy will apply to the following classes of NI contributions:

- Class 1 that are above the primary and secondary thresholds

- Class 1A and Class 1B for Employers

- Class 4 for those who are self employed

Additionally, from 6th April 2023 employers will have to pay contributions for those who are above the state pension age.

Below is a summary of what changes will take place.

2022-22 Tax Year

| National Insurance | Tax Year 2021-22 | Tax Year 2022-23 |

| Class 1 Employee | 12% | 13.25% |

| Class 1 Employee (above UEL) | 2% | 3.25% |

| Class 1 Employer | 13.8% | 15.05% |

| Class 1A 1B Employer | 13.8% | 15.05% |

| Class 4 Self Employed | 9% | 10.25% |

| Class 4 Self Employer (Higher rate) | 2% | 3.25% |

2023-24 Tax Year

NICs revert back to original rates

H&SC Levy is a separate item on payslip

| Tax Year 2023-24 | |

| Class 1 Employee | 12% |

| Class 1 Employee (above UEL) | 2% |

| Class 1 Employer | 13.8% |

| Class 1A 1B Employer | 13.8% |

| Class 4 Self Employed | 9% |

| Health and Social Care Levy | 1.25% |

If you would like more information or guidance on issues relating to the Health and Social Care Levy, please contact Michelle Henderson, Payroll Analyst and a member of AAB’s Integrated Employment Solutions team.

Find out more about AAB’s Payroll and Employment Taxes team.

How AAB can help

Payroll & Employment

Accurate, efficient handling of payroll functions and employment tax are fundamental to your success. We help you get them right – easing your workload, ensuring compliance in the UK and globally, and keeping your employees satisfied. Our comprehensive services for payroll and employment taxes address all these issues and help you operate efficiently, confidently and compliantly. Whatever the size of your business, from start-up to global player, all the services you require from us will be tailored to your specific needs and integrated to provide seamless support.

View our payroll & employment serviceRelated services