IR35 Consultation Launched

HMRC launched the long-awaited consultation into the “Off-payroll working rules from April 2020” for the private sector last week and is open for comment until 28th May 2019.

However, any misguided hopes we had that HMRC had listened to the widespread feedback from the initial announcement, learned from the Public Sector changes and were going to implement these into the private sector plans have been well and truly dashed!

Key points at a glance:

- Small client companies will be exempt (for the most part) with further work to be done on establishing “small” for non-limited entities.

- Decisions must be passed to the PSC via the end client or the agency (failure to do so will be penalised).

- The PSC will be given a mechanism to disagree with a decision (but that mechanism to be decided by the end client).

- CEST is here to stay, but hopefully with improvement.

Who will it apply to?

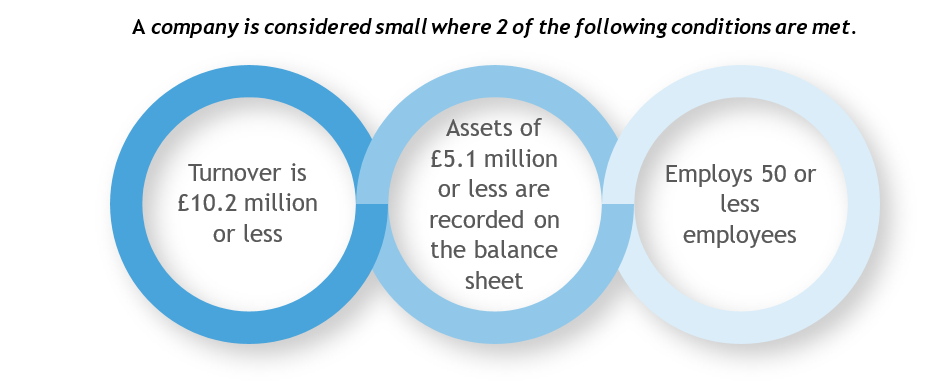

As mentioned in the previous consultation, the government proposes the legislation would not apply to all businesses in the private sector. It will seek to apply the legislation only to those engagements where the client organisation is not a small company as defined in the Companies Act 2006.

The consultation also discusses how this test might be applied to non-corporate entities and whether they should fall within the legislation if they exceed tests 1 or 3 above, or whether they need to exceed both 1 and 3 above.

Of critical importance is that it is anticipated the “small” test will apply to the ultimate end client (the place where the services are being provided) and not the agency in the chain; however, it is less clear what happens in situations where the client of the agency and the place where the services are provided are two different corporate entities. Logically, it would seem to follow that it is the entity that holds the contract with the agency that would be judged on this test but this may not be how HMRC view it.

In addition, the government will seek to implement anti-avoidance measures to counter any arrangements designed to ensure that parties connected to, associated with, or controlled by the end client cannot take advantage of the small company provisions and which seek to by-pass these qualifying conditions.

Client Decision

The public sector reforms have been widely criticised on the basis that there is no right for the individual PSC to be given the client decision as to whether IR35 applies and there is no appeal mechanism open to the individual contractor where there is disagreement with the client as to whether or not IR35 applies.

In this consultation, the government state “While the Government believes that the existing rules have worked adequately in the public sector, responses to the previous consultation identified a small number of points that would benefit from further consideration”.

The government proposes it would tackle these issues by:

- Information and transfer of liability. Including within the legislation an obligation that the decision, and reasoning, is cascaded to all parties in the chain. HMRC would see each party, respectively, responsible for passing the decision down the next party in the chain until it is received by the PSC. HMRC sees the transfer of debt – along the lines of the agency legislation – as a mechanism to ensure compliance.

- Including within the legislation a mechanism where a PSC can challenge the decision made by the end client organisation.

Information and transfer of liability

In respect of the first point above, the government is proposing that in order to “ensure compliance”, the liability under IR35, which would normally sit with the fee payer, may be moved to any party in the supply chain which has failed in its obligations to pass the Decision down the chain. This, in their view, would ensure all parties pass on the information.

Amidst these discussions, in the consultation, the government considers also that the legislation would provide a mechanism for HMRC to pass liability to another party in the supply chain in the event that the fee payer which primarily holds the liability “ceases to exist”. In these circumstances, HMRC proposes that the liability should transfer to the first agency in the chain (i.e. the one below the end client). If HMRC cannot collect from that agency, HMRC would ultimately seek payment from the end client.

Whilst we can see the need to ensure compliance, and can sympathise with HMRC being unable to obtain monies from liquidated companies, we consider that this could be fraught with problems in policing and could give rise to greater fears for all parties in the contractual chain that will attempt to be resolved with onerous provisions.

Right of Appeal?

In respect of the appeals process, the government considers that the easiest solution is “the introduction of a client-led status disagreement process”.

Effectively, end clients will have to develop and implement their own process to resolve disagreements with contractors based on a set of requirements detailed in legislation. How fair is this for the contractor when the party assessing the appeal is the same party that made the decision?

Many are arguing that this point is a clear indicator that HMRC are further outsourcing their tax collector role to the business community under the guise of legislative reform.

In addition, this will likely cause the most issues for clients, agencies and contractors alike. This could see the “disagreement process” being different for each and every engagement depending on the process created by each individual end client organisation.

Rather than providing clarity, we consider this will do nothing more than create further uncertainty and place all parties in the contractual chain in an impossible position. End clients will have to implement processes and undoubtedly hire staff, or expert advice, to facilitate this measure.

Agencies will have to keep abreast of the different mechanisms by which each of their client’s operates in respect of any disagreements. PSCs will then potentially find themselves going through a different process for every engagement with a new client.

The consultation does not indicate on what the parameters of this disagreement process should be. In order to be effective, there must be some consistency otherwise we could see situations where response times could vary from end client to end client. Moreover, at what point is the process deemed to be at an end – are contractors only entitled to one appeal?

Whilst in our opinion the appeals process is something which fundamentally had to be addressed given the lack thereof within the Public Sector, what is being proposed falls far short of what is required and does not seem well thought out.

Accounting and interaction with other legislation

The consultation continues by providing some much-needed clarification on accounting principles where the legislation applies and the interaction with other pieces of legislation. Interestingly, this legislation will take precedence over the Managed Service Companies legislation – this gives the effect that a Managed Service Company provider would see themselves primarily set aside in favour of the fee payer.

The consultation also makes it clear that IR35 takes precedence over the construction industry scheme.

CEST – no promises made

The consultation closes with assurance that HMRC’s CEST tool will be looked into and enhanced to ensure all parties have the resources they need to check their position. This is not an assurance which fills us with any confidence!

HMRC has imposed several high-profile retrospective tax bills on public sector freelancers off the back of CEST assessments, including more than 600 within the BBC. While this demonstrates the mistaken confidence that HMRC has in CEST and its ability to provide the correct IR35 status, it also poses doubts over whether updates to the tool will be made.

‘Exploring enhancements’ does not necessarily mean any changes will be made, and given HMRC’s belief in it, we wouldn’t be surprised if little changed.

However, should any changes be made, they need to happen at least six months before the rules are introduced in order to provide businesses with the time to understand and use them. HMRC cannot move the goalposts during the immediate build-up to the changes as it was this scenario which caused chaos in the public sector and more than likely contributed to the widespread blanket assessments.

More to come?

While this Consultation addresses some of the finer points of the mechanisms of applying this legislation, what have still not been addressed are the tests for determining whether IR35 applies. IR35 is effectively a test of self-employed status applied to a hypothetical arrangement – the government consulted last year on the tests of self-employed status and sought views on legislating or redefining the tests of self-employed status. The government’s published response to this consultation (which closed on 1 June 2018) remains notably absent.

As ever with HMRC, the consultation asks more questions than it provides answers.

If you would like further guidance on how the IR35 changes to the Private Sector will impact your business, please don’t hesitate to get in contact.

Find out more about our Payroll and Employment Taxes team.

How AAB can help

Payroll & Employment

Accurate, efficient handling of payroll functions and employment tax are fundamental to your success. We help you get them right – easing your workload, ensuring compliance in the UK and globally, and keeping your employees satisfied. Our comprehensive services for payroll and employment taxes address all these issues and help you operate efficiently, confidently and compliantly. Whatever the size of your business, from start-up to global player, all the services you require from us will be tailored to your specific needs and integrated to provide seamless support.

View our payroll & employment serviceRelated services