Important VAT Changes – Construction Reverse Charge

Important VAT Changes – Construction Reverse Charge

1 October 2019 will see significant VAT changes within the construction industry. In an effort to combat perceived abuses in the sector, a domestic “construction reverse charge” rule is being introduced which will change who is responsible for accounting for VAT in relation to certain supplies of construction services. In particular, supplies between sub-contractors and main contractors will be impacted by these changes.

The new rules will catch a broad range of construction services, including those of builders, joiners, electricians, plumbers, painters, air conditioning installers and many ground workers.

How do the rules currently work?

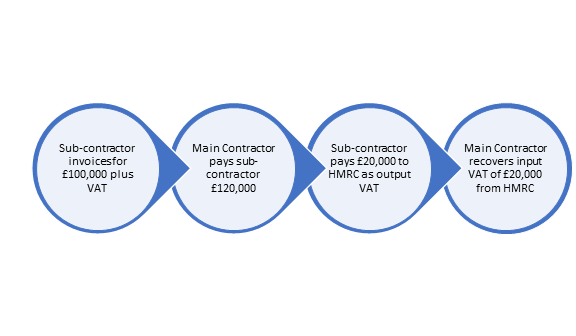

As with other domestic supplies of services, the sub-contractor (as the supplier) is responsible for charging and accounting for VAT to HMRC on supplies of construction services. The main contractor (as customer) pays the VAT to the sub-contractor and recovers this from HMRC.

Provided that both the sub-contractor and main contractor are legitimate businesses, this process works. However, HMRC is concerned about the current levels of “missing trader fraud”. Under a missing trader scenario, the sub-contractor charges and collects the VAT due from their customer before disappearing without declaring and paying the VAT due over to HMRC.

What are the new rules?

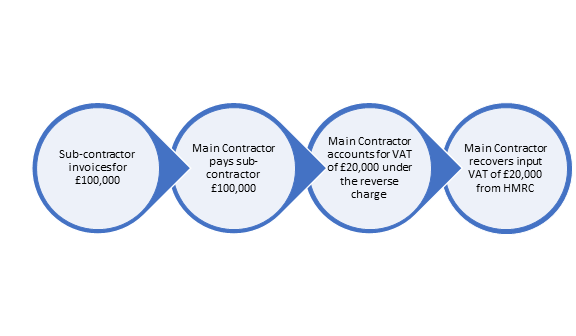

To combat missing trader fraud, HMRC propose to pass the responsibility to account for the VAT to the customer. Consequently, from 1 October 2019, the main contractor will be responsible for declaring the VAT on supplies received from the sub-contractor under the “reverse charge” rules. The main contractor can still recover the self-assessed VAT subject to the normal rules.

This is best illustrated with an example:

Current Position:

Revised position:

Are all supplies in the construction sector caught by these new rules?

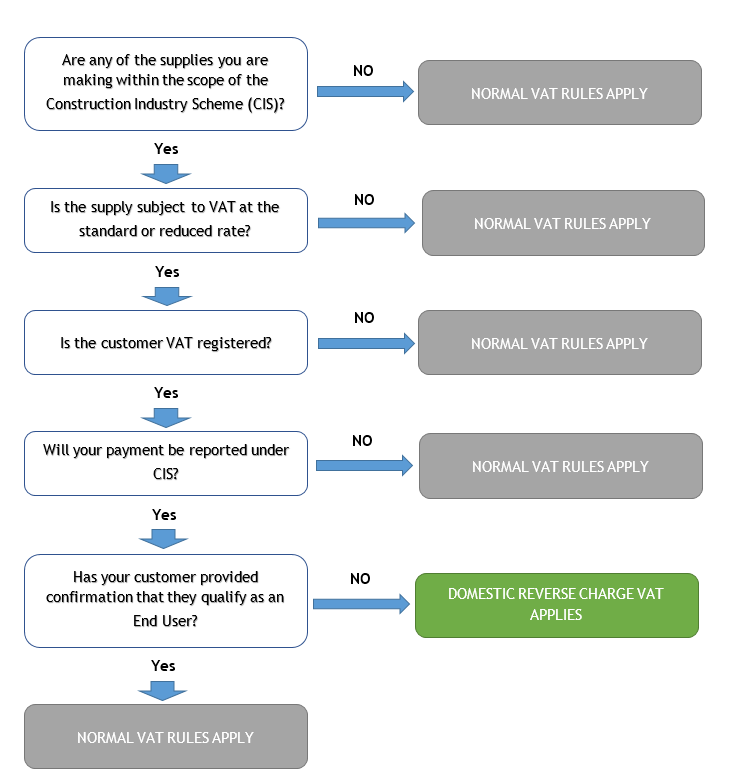

Not all supplies within the construction industry will be covered by the new rules. In summary, the domestic reverse charge will only apply to supplies at the standard or reduced rate of VAT where payments are required to be reported through the Construction Industry Scheme (CIS).

The new rules will apply to a wide range of construction services including:

- General construction;

- Repairs, renovations and maintenance services;

- Cleaning services;

- Painting and decorating services;

- Heating, ventilation and air-conditioning services;

- Groundwork services.

However, as the new rules only apply to construction services falling under CIS on which VAT is charged, the following construction services will still be accounted for under the normal rules:

- Supplies to the final customer (“End Users”);

- Zero-rated supplies (e.g. services in the course of construction of a new dwelling)

In addition, the following activities will not be caught by the new rules:

- Certain supplies between connected companies;

- Certain supplies between landlord and tenant;

- Drilling for and extraction of natural resources, and the construction of tunnels, boring or other underground works for this purpose;

- Professional services provided by architects, surveyors and other consultants;

- The manufacture of certain building or engineering equipment and components;

- The installation of seating, blinds and shutters;

- The installation of security systems, burglar alarms, CCTV and PA systems.

The following flow chart sets out the rules for the application of the reverse charge to building and construction services:

What should businesses in the construction industry do to prepare for the changes?

A key challenge for businesses will be getting their systems in place to be able to deal with the new rules. The biggest burden will be businesses that act as a sub-contractor, main contractors and also as an End User.

For sub-contractors, as construction services can potentially be subject to VAT at 0%, 5% or 20%, they need to have processes in place to ensure the correct VAT treatment is applied. In addition, they will have to consider the cashflow implications where they have previously used the VAT collected from customers as working capital before they need to pay this to HMRC.

For main contractors, particularly those that use a lot of sub-contractors, they will need to have processes in place to understand when they are required to account for the VAT due.

End users, and any other business not caught by the new rules, will need to confirm their status to their suppliers and confirm that they are exempt from the construction reverse charge.

Consequently, all businesses involved in the construction industry should review their supply chains to consider how they will be impacted by the changes and ensure that they have the necessary systems and controls in place.

If you would like to discuss how the upcoming changes will affect you, please get in touch with Alistair Duncan (alistair.duncan@aab.uk) or your usual AAB contact.